How to Choose Between Venture Debt Financing, Equity for Growing your Business

Choosing between venture debt financing and equity capital for a growing company can be a difficult balancing act. Both options have tradeoffs that make choosing the “right” option a very personal choice for your business.

To explore these tradeoffs, let’s look at the example of Grab, a transportation and finance business based in Singapore, that focused on fueling their growth through equity raises. Since it was founded in 2012, the company has raised $12.2B, and while a portion of that was debt, the vast majority of their funds came from equity. With a $39.6B SPAC deal in the works, many would say the company found success with its fundraising strategy.

But at this point, the executive team owns less than 4% of the company they created. That means that as the company continues to thrive, the founding team is getting far less than they could have had they grown the company by raising venture debt financing instead. If you did the math, you’d likely find that the company could’ve safely taken on potentially billions in debt, reducing dilution for the executive team and employees — ensuring they’d keep more of the upside coming out of the upcoming liquidity event. Thinking through this math while fundraising could have earned Grab employees hundreds of millions of dollars of additional personal wealth.

So why didn’t Grab choose to raise debt? While we don’t know what happened on the inside, it’s clear that a lot of companies struggle to accurately assess the risks of taking on debt. A recent study in the U.S. found that nearly 50% of entrepreneurs reported regretting using equity when venture debt was available, and 90% agreed that venture debt is an under-discussed financing option. This means that in many cases, companies may be taking far more equity funding than they need to, which can be less risky but reduces the potential reward for current shareholders.

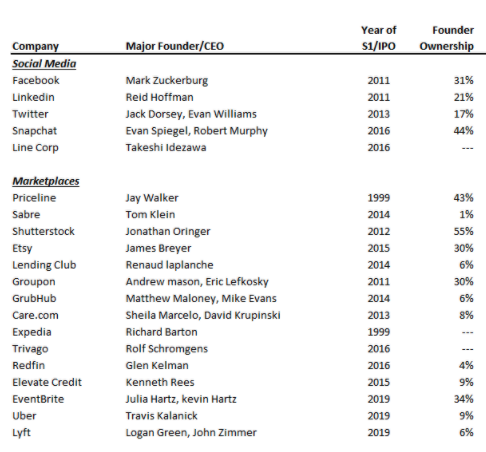

Moreover, as Sammy Abdullah has brilliantly laid out, founders in the same industries often have wildly different exit ownership percentages of their companies. Does it make any sense that the Twitter co-founders owned ⅔ less of their business than the Snapchat co-founders? What about the Dropbox founders owning 9x more of their company than the Box co-founders?

Planning around dilution is rarely discussed as entrepreneurs grow their business but, as the above examples show, it can be more important than key product launches or major customer wins. The good news is that this is low-hanging fruit available to any entrepreneur so let’s dig in.

Mitigating dilution is about making predictable progress or using debt

There are two ways to mitigate dilution:

1) Make predictable operational progress — If you are able to craft a plan that gets you to major traction inflection points efficiently, each time you need to raise capital, you can do so at materially higher valuations. This was the difference between Twitter and Snapchat. Twitter famously started as a podcasting service called Odeo. While the pivot to Twitter was a much admired act of entrepreneurial grit, starting in the wrong business meant dilution for the founders who needed to raise money at points in the journey where there was not yet evidence of product-market fit.

Snapchat, on the other hand, launched from a Stanford dorm room, hit the market perfectly on day one. There were no pivots, down rounds or recaps and correspondingly the founders owned 44% of the business at IPO vs. 17% for the Twitter founders.

2) Use debt to fuel non-dilutive growth — Making predictable progress is not always possible – whether due to complex R&D or evolving market dynamics. All entrepreneurs, however, can use debt to limit dilution so long as they thoughtfully quantify the risk of doing so. So how do you assess the risk of taking on debt?

Assessing the risk / return balance for debt and equity financing

Risk is a fundamental factor driving which kind of financing is right for your company at any given time. As venture equity is the lower-risk option for early-stage businesses, because it does not have to be paid back, debt financing is where you’ll most need to evaluate risk. Assessing the risk of taking on debt is remarkably easy: just calculate the worst-case operating scenario for your business. Then calculate whether you can comfortably repay debt even in this scenario. If you can, then debt makes sense for you.

Afterall, this is how most consumers think about their mortgage. Most consumers don’t expect their home value to fall to zero requiring them to repay their mortgage overnight. This is not a realistic downside case. Instead, they may envision a scenario where home values contract by 15% and it takes them 6 months to find a new job – a much more realistic case. With enough savings to cover the job transition and a 20% down payment in place, this is a safe downside scenario.

It is possible to calculate the same for your business by answering questions like:

- How much have my churn rates spiked historically and how long did this last?

- How does churn work during recessions in my industry?

- Are there suppliers that can drive up my operating costs rapidly? If this happened, how long would it take for me to find a new supplier at a more reasonable cost?

With a few simple questions answered empirically from your data and relevant macroeconomic data to your industry, you can know with high certainty whether your business can take on debt.

If you can take on debt, what’s the upside?

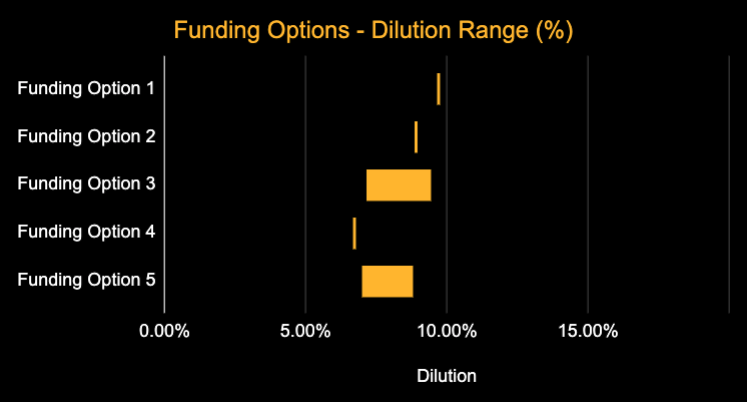

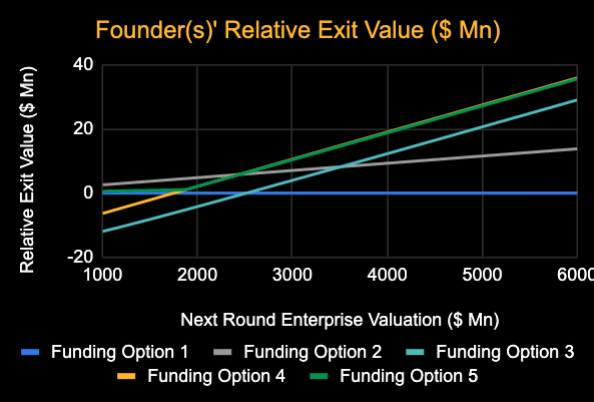

A thoughtful analysis of financing options should consider dilution and its results on wealth. For example:

With a clear picture of the upside and downside of debt, you can confidently move forward financing your business for success.

So how do I take advantage of debt?

The analysis we discussed can be done in two ways. Either by a stellar in-house finance team or by using a tool like Hum’s Intelligent Capital Market to scenario analyze your business and plan financings. Either way, you want to get clarity on these key questions before moving forward.

Once you have that clarity, then it’s about execution – reaching out to investors and showing them the story your data already tells whether you use a neutral 3rd party like Hum or reach out yourself.

Feel free to contact us 429 if you’d like additional help assessing the tradeoffs between taking venture capital or debt in your business.